|

Click to listen to this article

|

According to the latest AgWest Farm Credit report, potato markets remain under pressure as persistent supply-demand imbalances weigh on the industry. Demand for frozen potato products and table potatoes has softened, following several years of relatively flat consumption. At the same time, processing capacity has expanded, contributing to an ongoing oversupply environment.

Export markets remain critical to absorbing excess domestic production, but U.S. competitiveness has been challenged by a strong dollar and intensifying competition from global suppliers. In the first quarter of 2026, U.S. frozen potato product exports declined 12.8%, largely driven by a notable drop in frozen French fry purchases.

Weaker demand and rising costs continue to weigh heavily on the potato sector. Reduced contracted acres, ongoing water concerns and elevated production expenses are contributing to declining planted acres across AgWest’s territory.

Industry estimates suggest Washington acreage could fall to its lowest level since the early 2000s, while Idaho is expected to have approximately 15,000 fewer planted acres. These reductions reflect ongoing financial strain.

While tighter production can often provide price relief, this seems unlikely for potato growers this year. Despite reduced plantings, processors are carrying over inventory from the 2025 crop, limiting upward price potential. Even with fewer planted acres, above-trend yields and sustained reduction in demand could sustain oversupply conditions and prolong the current period of pricing pressure.

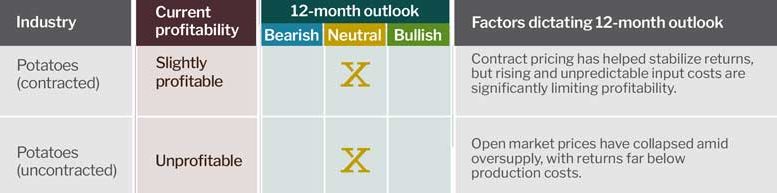

Profitability

Potatoes (contracted): Slightly profitable – Neutral 12-month outlook

Potatoes (uncontracted): Unprofitable – Neutral 12-month outlook

Contract pricing has helped stabilize returns, but rising and unpredictable input costs are significantly limiting profitability.

Open market prices have collapsed amid oversupply, with returns far below production costs.