|

Click to listen to this article

|

By Ben Eborn, Publisher, North American Potato Market News

U.S. potato production in the reporting states is currently expected to match production from the 2024 crop, according to North American Potato Market News’ (NAPMN) estimate as of press time. Though overall production is expected to be relatively stable this year, there have been some significant shifts in production intended for each of the industry sectors.

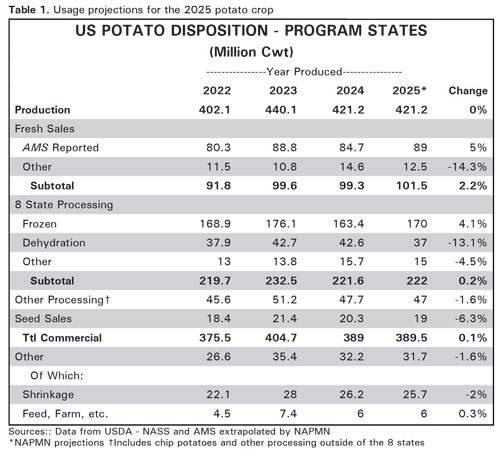

Table 1 outlines our current usage projections for the 2025 crop, along with a three-year history of usage, as reported by USDA. Please note that relative demand between the industry sectors and market forces could alter the distribution of the 2025 potato crop, relative to our current outlook. In the remainder of this article, we lay out our projections for the various industry sectors in greater detail.

Table Potatoes

Program states shipped 84.7 million cwt of table potatoes from the 2024 crop. That is 4.1 million cwt less than they shipped a year earlier. We believe that supply conditions and market forces will support a 4.3 million cwt increase in 2025 crop-year shipments, to 89 million cwt, a 5% increase. We expect most of the increase in table potato sales to come from Idaho, where some growers planted table potato varieties after receiving processing potato contract reductions.

In addition to increased sales, the product mix could shift toward russets again this year. Low prices and an increase in supply could boost russet table potato movement, which will likely offset red potato sales and possibly yellow potato sales. Early-season red potato shipments are down 22.8% from a year earlier. Red potato shipments will likely fall short of the 2024-25 pace throughout the storage season. Early-season yellow potato shipments are running 2.6% behind last year’s pace. Yellow potato shipments from the storage states could be relatively flat this year.

The russet supply situation is complicated by its intersection with the processing industry. Early russet table potato shipments have been running 7.2% ahead of the 2024 pace. Most of the increased movement is from Idaho. However, shipments have slowed down recently. Packers shipped 1.09 million cwt of russet table potatoes during the week ending Sept. 27. That is 36,000 cwt more than the previous year’s shipments, a 3.4% increase. The Idaho Grower Returns Index fell to $3.10 per cwt by Oct. 1, compared to $7.86 per cwt a year earlier. Fresh shippers from other areas are struggling to compete with those prices. We expect strong russet table potato movement and poor open-market prices throughout most of the season.

Frozen Processing

Processors in the eight reporting states used 163.4 million cwt of potatoes from the 2024 crop for frozen processing. That is 12.7 million cwt less than year-earlier usage, a 7.2% downturn.NAPMN expects fryers to use 170 million cwt of potatoes from the 2025 crop. That is 6.6 million cwt more than last year’s reported usage, a 4.1% increase. We believe the expected increase will be supported by relatively strong domestic and export demand for French fries and other frozen potato products. North American fryers shipped 2.6% more frozen potato products to offshore markets during the year ending June 30 than they did a year earlier. However, North American fryers will likely face strong competition from the European Union and other exporters during the 2025-26 processing season. Global French fry exports have grown by an average of 4.4% per year during the past 10 years.

Despite significant contract reductions for the 2025 crop, we believe that raw product supplies will be abundant again this year due to strong yields in most of the major processing regions. Though local supplies could be tight for processors in the Atlantic Northeast, potatoes may be imported from other regions to cover any supply gaps. North American fryers have expanded their processing capacity during the past several years. If fryers choose to pull potatoes from the table potato pile, processing use for the 2025 crop could exceed our estimate.

Dehydration

Dehydrators in the reporting states used 42.6 million cwt of potatoes from the 2024 crop. That nearly matched the year-earlier volume, according to USDA reports. We expect dehydrators in the eight reporting states to use 37 million cwt of potatoes from the 2025 crop. That is 5.6 million cwt less than they used from the 2024 crop, a 13.1% reduction. It falls 4 million cwt below the three-year average pace, but it is only 853,000 cwt less than 2022-crop usage.

Though we do not have reliable data for domestic dehydrated product sales, offshore sales have been sluggish. Reported U.S. potato flake exports during the year ending July 31 fell 30.8% short of the previous year’s sales volume. That was the smallest U.S. potato flake export volume for the period since 2009-10. Most of the U.S. dehy processing capacity is in Idaho. However, growers in Idaho and across the country indicate that there is currently very little dehydrator demand for off-grade potatoes. Dehydrators have made significant contract reductions for both field-delivery and storage potatoes from the 2025 crop. Dehy processing use could fall short of our estimate if finished-product demand does not pick up.

Other Eight States Processing Use

This is the difference between total processing use reported for the eight states and usage reported for dehydration and frozen products. It may include usage at chip plants in the reporting states, as well as other miscellaneous uses. At 15 million cwt, usage in this category would fall by 4.5%.

Other Processing Use

This is the difference between total processing use reported for the program states and usage reported for the eight processing states. This is where most of the program states’ chip potato usage would show up. At 47 million cwt, we are projecting a 747,000 cwt reduction in 2025-crop processing use outside of the eight reporting states. Despite the 1.6% decline, projected usage in this category exceeds 2022 levels. Chip potato usage could exceed our estimate if storage supplies are sufficient to offset the need for early new-crop potatoes.

Seed Potatoes

Reported seed potato shipments from the 2024 crop totaled 20.3 million cwt, down 5.3% from the previous year. Three years of poor prices, due to excess supplies of table and processing potatoes, should encourage acreage reductions in 2026. At 19 million cwt, NAPMN expects seed movement from the program states to decline by 6.3% relative to the 2024 crop.