|

Click to listen to this article

|

By Ben Eborn, Publisher, North American Potato Market News

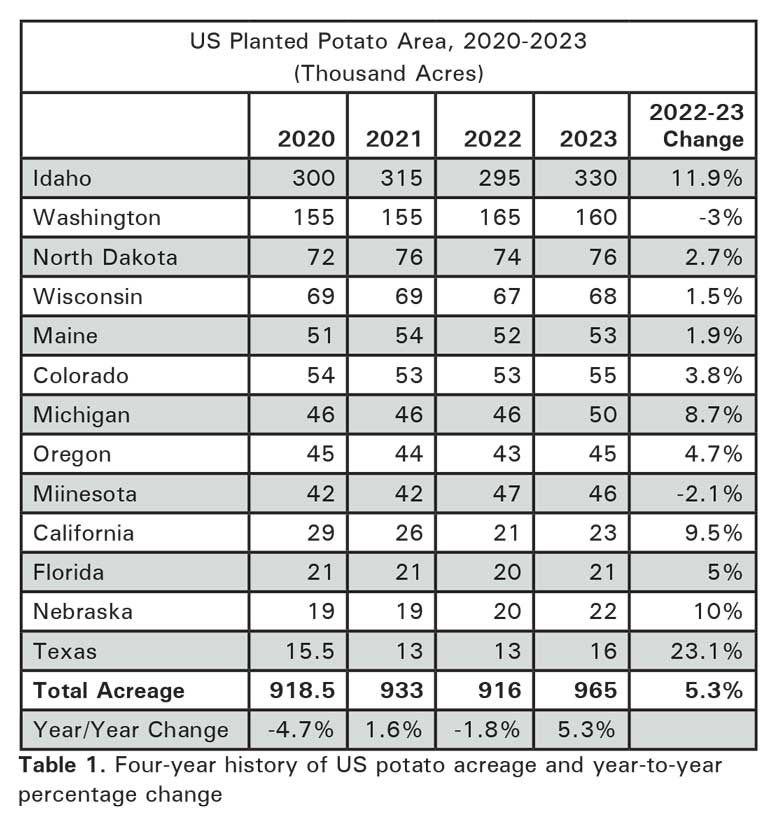

Factors affecting 2024 potato acreage are mixed. Growers have many things to consider when making planting decisions for this year’s potato crop. Some of the major factors include current and projected potato prices, prices for alternative crops, production costs, contract volumes, irrigation water supplies, land availability and crop rotations. Table 1 shows a four-year history of U.S. potato acreage by state, along with the year-to-year percentage change. In this article, we review some of the key factors influencing 2024 planting decisions.

Alternative Crop Prices

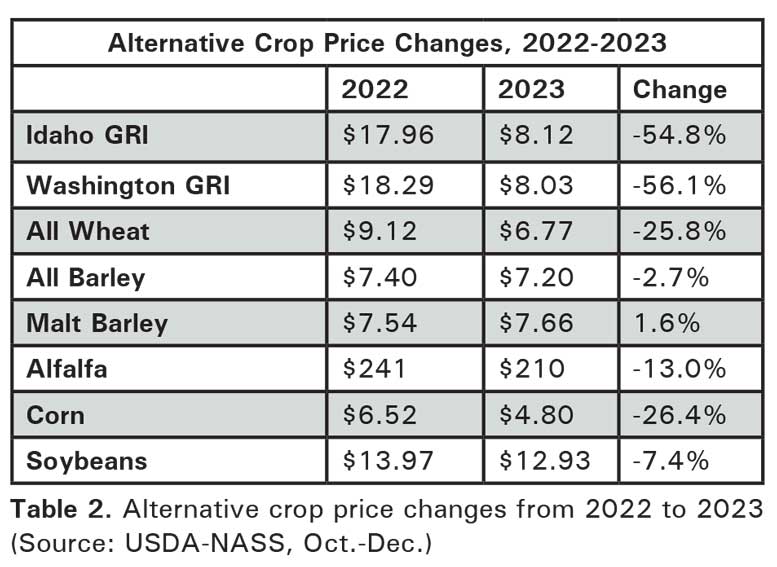

Near breakeven open-market prices for the 2023 potato crop could encourage growers to plant fewer acres to potatoes in 2024. The average Idaho Russet Grower Return Index from October through December is $8.12 per cwt, down 54.8 percent from $17.96 per cwt a year earlier. The Washington GRI averaged $8.03 per cwt during the same timeframe, down 56.1 percent from the previous year.

Prices for most competing crops are also down from where they were a year ago. USDA reports that the national all-wheat price averaged $6.77 per bushel during the October-December period versus $9.12 per bushel a year ago, a 25.8 percent decline. All-barley (-2.7 percent) and malting barley (+1.6 percent) prices are relatively flat. Alfalfa prices are down 13 percent across the country at $210 per ton. Corn prices have dropped 26.4 percent to $4.80 per bushel, while soybean prices have fallen 7.4 percent to $12.93 per bushel. Growers may consider potato acreage cuts this year, especially given the relatively stronger prices and lower input requirements for alternative crops.

Production Costs

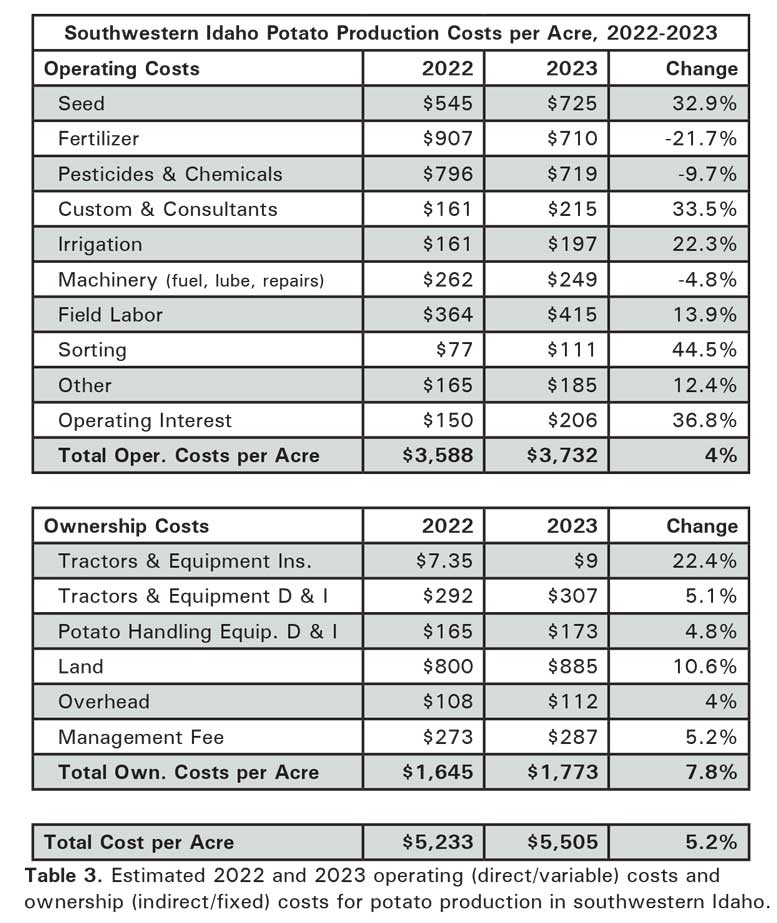

Though prices for some inputs could come down this year, overall production costs are expected to remain high for the 2024 crop. Table 3 shows the estimated 2022 and 2023 operating (direct/variable) costs and ownership (indirect/fixed) costs for potato production in southwestern Idaho. Per acre operating costs rose by 4 percent. There were significant cost increases last year for seed, custom and consultants, irrigation and labor. On the other hand, fertilizer, chemical and fuel prices were down from 2022 levels. Currently, seed, fuel, chemical and fertilizer costs are below year-earlier levels. Other operating expenses are expected to increase in 2024. Labor costs are likely to continue upward with rising inflation. Relatively high interest rates could decline somewhat, but probably not before operating loans are secured.

Ownership costs are on the rise. Land rent and equipment costs will increase again this year. Overall, 2023 ownership costs climbed 7.8 percent above 2022 costs, which put the total cost increase at 5.2 percent. Total production costs climbed as much as 8.8 percent in other parts of Idaho. Other growing areas faced similar increases. Idaho’s cost per cwt was down slightly due to the 2023-crop yield increases. Machinery and equipment depreciation has been increasing with rising equipment and interest costs. A shift to mechanical sorting due to rising labor costs and workforce availability has encouraged more investment in technology. Land rents continue to receive upward pressure as farmland values increase along with demand from other ag sectors.

Other Factors

Several other factors could affect the 2024 U.S. potato acreage. Processing contract volumes in the Pacific Northwest are expected to be down, following last year’s large production increase. Carryover from the 2023 crop will reduce the need for early potatoes. Contract volumes may be more stable in the Midwest and Northeastern processing states. On the bright side, both domestic and export demand for French fries and other frozen products has been strong. Crop rotation requirements typically prevent wide year-to-year swings in potato acreage. Shifts in acreage on a statewide basis are often more variable than the change in acreage on a national level. Year-to-year changes are typically less than 5 percent. Finally, the country’s overall economic and political conditions may also weigh heavily on planting decisions. Growers across the country are considering the unique financial, production and market risks of growing potatoes this year.

Summary

There are several factors to consider when making planting decisions. Open-market potato prices are down significantly compared to the past two years. Prices for most alternative crops are also down, but not as much. The opportunity cost of growing potatoes versus other crops will be at the forefront of this year’s planting decisions. Rising production costs could continue to squeeze profit margins. Even with relatively flat contract prices, profit margins could be slim unless growers monitor costs closely. Other factors such as contract volumes, irrigation water supplies, yield variation, crop rotations and national economic conditions will play into planting decisions this spring.